Doing Business in the Middle East:

Top 10 risks and opportunities in 2013 and beyond – Oil and Gas Sector

By Ernst & Young

Overview:

In line with our 2020 vision of “building a better working world”, Ernst & Young (EY) strives to make a difference by helping our people, our clients and our wider communities to achieve their potential. We regularly present our continuous research and reports that help businesses to identify risks, exploit opportunities and anticipate future trends and patterns.

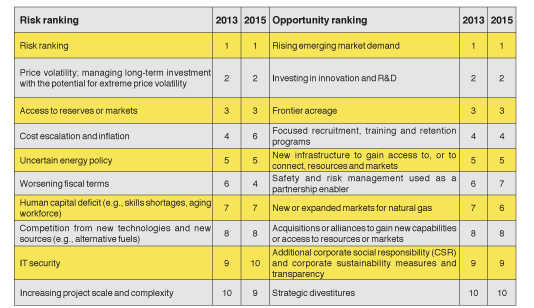

Based on a large sample survey of companies in 21 countries, and across various industry sectors, EY identified a top 10 list of risks and opportunities, many of which are interlinked. Each ranked risk and opportunity was then discussed with relevant business executives and EY specialists, to gather the insights and perspectives upon which the findings are based.

Business Pulse: Exploring dual perspectives on the top 10 risks and opportunities in 2013 and beyond – Oil and Gas Report

This report takes the pulse of current thinking, insights and expectations from industry executives and EY specialists providing an industry overview of the top 10 risks and opportunities. While every oil and gas business has their risk and opportunity profile, businesses may also classify risks and opportunities on different basis than has been considered for the report; yet oil and gas businesses can use the discussion of the risks and opportunities in the report to assist in the process of defining and ranking their individual company priorities.

The research shows, unsurprisingly, that health, safety and the environment (HSE), regulatory compliance, price volatility and the increasing challenge associated with accessing reserves and the markets take the top spots. A new entrant to the top 10 this year is IT security, specifically the threat to companies’ operations or indeed, country and region-wide energy infrastructure —by cyber-attacks or cyber theft of their intellectual property.

With regard to opportunities, rising emerging market demand is this year’s number one, rising three places since our 2011 report. With the continued growth of the world’s emerging economies, energy demand in these countries will also rise rapidly, and the opportunity for oil and gas companies to take advantage of this is immense. The opportunity list saw many new entrants this year, including new infrastructure to gain access to or connect to resources and markets, safety and risk management used as a partnership enabler, and new or expanded markets for natural gas.

The presentation of results and rankings this year was different; where the top 10 rankings as in the past, but for the main section of the report, opportunities and risks with clear links have now been clustered and discussed as a combined narrative. In so doing, EY has identified three clusters, or themes, into which the top 10 risks and opportunities fall: interaction with governments and regulatory bodies, core business focus and counterparty risk management, and the pace of technological change. These clusters of risks and opportunities are previewed in the following section, to give an overview and a dual perspective on the themes contained within them.

Interaction with governments and regulatory bodies

Rich rewards for engagement and transparency

The supply chains in the oil and gas sector are increasingly interconnected. Managing them against a backdrop of multiple governments with different and changing policies and regulations is challenging enough. The industry is also moving quickly into new geographical and technical areas. These create new challenges for governments, and short time frames in which to make critical decisions that have some very profound, long-term implications for oil and gas companies

Regulatory compliance is a challenge in any industry, but the circumstances of many oil and gas companies make it a unique discipline. New method of extraction, such as hydraulic fracturing, present risks to regulators who are unsure of the wider impact of their large-scale use. Gaining approval from individual jurisdictions to develop reserves requires an appreciation of the specific circumstances involved in each case. Companies must take into account the competing interests and priorities of government, which all have political or economic imperatives to consider. A positive public image can help in this regard; companies must ensure that governments will want to be seen doing business with them.

Core business focus and counterparty risk management

Covering your bases

With the inherent complexity and capital-intensive nature of the oil and gas industry, joint ventures are commonplace, as are multiple, complex supplier relationships. These partnerships are generally fruitful, but carry a number of intrinsic risks.

The reliance on joint venture and contracting partners has been pulled into sharp focus by the 2010 Gulf of Mexico spill. The incident demonstrated the considerable financial and reputational risk to which all parties are exposed. With high numbers of joint ventures and third-party service providers, the issue of partner and contractor assessment and management has now moved up the agenda for all leading oil companies and investors. Non-operated joint venture stakeholdings are a particular concern, as they tend to combine a limited ability to influence and control day-to-day operations with considerable exposure should things go wrong.

Companies are thinking hard about their core business focus, and many are recognising that they cannot be present in all countries in all activities. With opportunities outweighing the capital and skilled resources that most companies are able to invest, they have to be clear about where their organisation’s core competencies lie and where they can achieve the greatest returns. This is having a dramatic restructuring effect on the global energy landscape and on how companies manage their own risk and limit their exposure to partner’s risk.

The pace of technological change

Staying ahead of the game

For the oil and gas industry, technological change primarily concerns new ways of accessing and distributing natural resources. There are significant opportunities for oil and gas companies looking to utilize new technology to identify and extract hydrocarbon resources and to lower their supply chain costs. However, for companies looking to develop or take advantage of new technologies, significant investment is required to develop and maintain an up-to-date understanding of industry trends. Additionally, companies need to assess the potential benefits for their business of technological development across a broad range of other industries.

Elsewhere, technological change means a greater role for IT and management and control systems within the industry. While the benefits are apparent, the risks and costs are also substantial.

At a time when major capital investment decisions need to be made over a 20-to-30-year horizon, the industry faces the difficult task of trying to predict not only how technology will impact and drive our future energy consumption and supply, but how it will change day-to-day operations, drive cost savings and enable new sources of energy to be commercialised.

Emerging challenges

While this report takes the pulse of the oil and gas landscape in 2013, EY research has identified the importance of keeping up with technological progress. Although the challenges oil and gas companies face over the next decade are uncertain, EY has yet been able to identify three additional areas in which current trends could present both risk and opportunity to companies in this time frame.

The first is access to finance and capital market constraints. Oil and gas developments are becoming increasingly challenging, complex and expensive. Consequently, the risks associated with raising capital are likely to intensify.

The second challenge is the trend toward increasingly tight local content requirements. Should this trend continue, it will have implications across a range of issues, including labor costs and the ability to deliver projects on challenging time schedules.

The third area is catastrophic environmental events. Should these become increasingly common or inextricably linked to CO2 emissions, then the argument for immediate action to reduce CO2 emissions will become not just about affordability, but necessity.